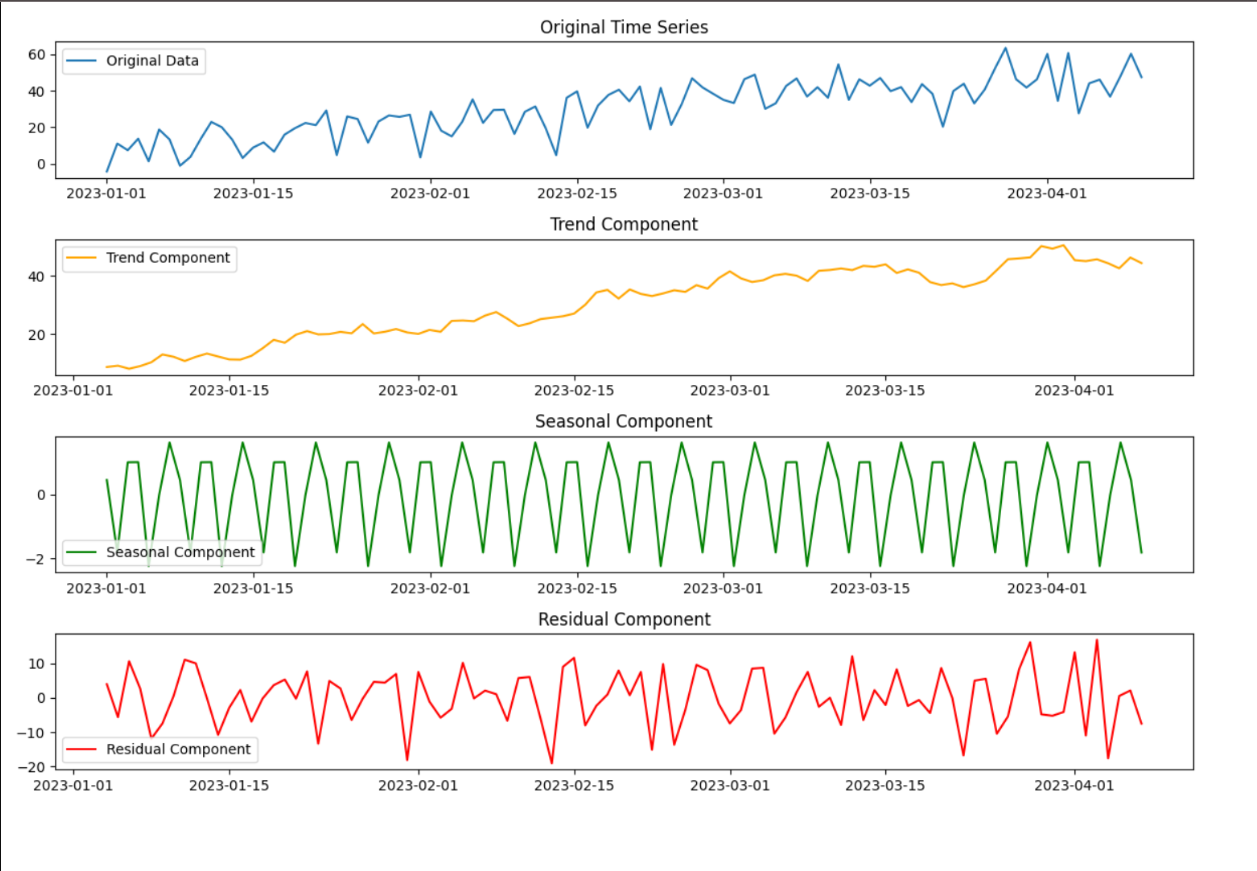

Sales Forecasting (Time-Series)

Predict weekly sales across products & locations using classical + ML models; enable inventory and promo planning.

Overview

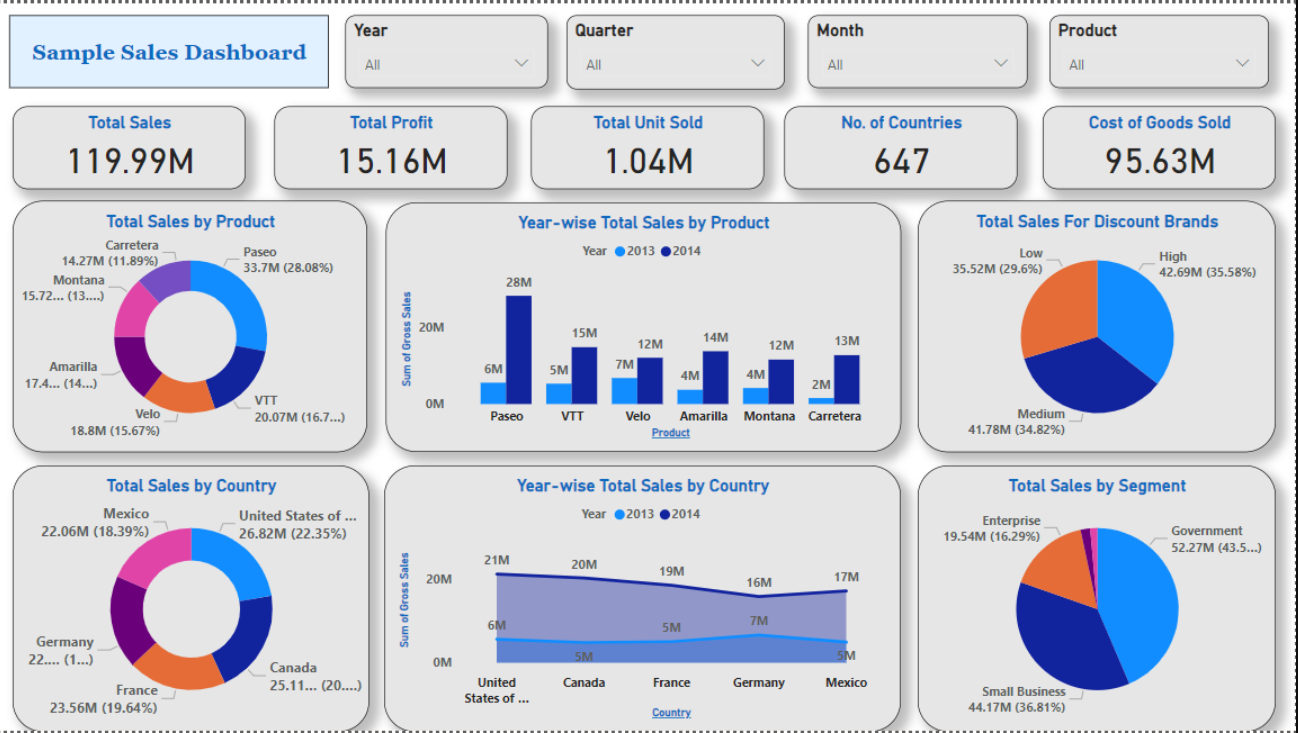

We built a forecasting pipeline that learns seasonality, promotions, holidays, and price elasticity to predict weekly sales per product–location. A Power BI dashboard visualizes forecasts, uncertainty, and bias, helping planners align inventory and campaigns.

Time-Series CV

Lag/Window Features

Hierarchical Aggregation

Deployment to BI

Data

- Grain: weekly product × store (3–5 years history)

- Signals: calendar, holidays, promos, prices, weather, stockouts

- Targets: units and/or revenue; forecast horizon typically 8–12 weeks

Approach

- Baselines: Naïve, seasonal naïve, ETS.

- Classical: SARIMA / Prophet for strong weekly/annual seasonality.

- ML: Gradient boosting (XGBoost) with lags, rolling means, promo/price features.

- Validation: Rolling-origin time-series CV; metrics: MAPE/WAPE/sMAPE/RMSE.

- Ensemble: Blend classical + ML per series based on validation rank.

# sketch: lag/window features for ML

def add_lag_feats(df, lags=(1,2,3,4,5,6,7,14,28), windows=(7,28)):

for L in lags:

df[f"y_lag_{L}"] = df.groupby(["store","sku"])["y"].shift(L)

for W in windows:

df[f"y_ma_{W}"] = (df.groupby(["store","sku"])["y"]

.shift(1).rolling(W, min_periods=1).mean())

return df

# sketch: rolling-origin cross-validation

def rolling_cv(df, n_folds=4, horizon=8):

folds = []

end = df["ds"].max()

for k in range(n_folds):

cutoff = end - pd.Timedelta(weeks=(n_folds-k)*horizon)

tr = df[df["ds"] <= cutoff]

va = df[(df["ds"] > cutoff) & (df["ds"] <= cutoff + pd.Timedelta(weeks=horizon))]

folds.append((tr, va))

return folds

↓ 27%

MAPE vs baseline

↓ 18%

WAPE vs last season

± 9.3%

Avg. forecast band

Architecture (simplified)

Jobs scheduled; forecasts published to BI with versioned artifacts.

Tech Stack

Python · Pandas · Prophet / SARIMA · XGBoost · scikit-learn · Power BI · (optional) Power Automate